You’re about to sign a document that puts your house, your savings, and your spouse’s financial future on the line. The SBA loan officer will hand it to you in a stack of 40 other forms and act like it’s routine. It’s not. Here’s what you’re actually agreeing to — and how to make the risk manageable.

You found the HVAC company. The numbers look right. Revenue is $1.8M, SDE is $350K, the service agreement book is solid, and the seller isn’t trying to sell you a story. Your SBA lender says you’re approved for a $900K 7(a) loan.

Then the loan package arrives and buried on page 31 is a document titled “Unconditional Personal Guarantee.”

You read it. Or you don’t — most people don’t, and that’s a problem. Because that single page means more to your financial life than anything else in the stack. It means that if this business fails, you don’t just lose the business. You lose whatever they can find with your name on it.

I signed one of these twenty-two years ago. I’d do it again for that deal. But I wish someone had sat me down and explained exactly what I was agreeing to, because the lender sure wasn’t going to.

What a Personal Guarantee Actually Is (And Why the SBA Requires It)

A personal guarantee is exactly what it sounds like: you personally guarantee that the loan will be repaid. Not the business. Not your LLC. You. The human being with a Social Security number and a house and a checking account.

Here’s the chain of liability in an SBA 7(a) loan:

- The lender issues the loan to your business

- The SBA guarantees 75–85% of that loan to the lender (meaning the bank gets paid even if you default)

- You guarantee the full amount to the SBA (meaning the government comes after you to recover what they paid the bank)

The SBA isn’t lending you money out of generosity. They’re backstopping the bank’s risk, and they need someone to backstop theirs. That someone is you.

The 20% ownership rule

Anyone who owns 20% or more of the business must sign a personal guarantee. No exceptions. Buying with a partner who’s putting in 25%? They sign too. Your spouse owns half the LLC? They sign.

This isn’t negotiable at the SBA level. The lender can’t waive it. Your attorney can’t talk them out of it. It’s baked into the program requirements.

Unlimited vs. limited guarantees

Most SBA personal guarantees are unlimited, meaning there is no cap on what you could owe. The full loan balance plus accrued interest, fees, and collection costs. If you owe $750K, you owe $750K.

Some conventional loans offer limited guarantees — capped at a percentage or a dollar amount. SBA loans almost never do. Know which one you’re signing.

Key Warning: The personal guarantee survives the life of the loan. Even if you sell the business or transfer ownership, the guarantee remains in effect until the loan is fully repaid or the lender releases you in writing. Selling the company does not automatically release your guarantee.

What Assets Are Actually on the Line

When you sign an unlimited personal guarantee, you’re essentially handing the lender a map to everything you own. Here’s what’s exposed.

Your home

This is the big one. If you own a house — or you’re paying a mortgage on one — it’s on the table. The lender can place a lien on your home and, if necessary, force a sale to satisfy the debt.

Common misconceptions:

- “My house is in a trust.” A revocable living trust does not protect your home from creditors. If you can revoke the trust, they can reach the asset.

- “My house is only in my spouse’s name.” Depends on your state. In community property states, marital assets are jointly owned regardless of whose name is on the deed. More on this below.

- “I have a homestead exemption.” You might. It varies wildly by state and it matters — but it protects equity, not the whole house. We’ll cover this in the mitigation section.

Savings and retirement accounts

Your checking account, savings account, money market funds, brokerage accounts — all exposed. Retirement accounts get more nuanced:

- 401(k) and IRA accounts are generally protected from creditors under federal law (ERISA for 401k, the Bankruptcy Abuse Prevention Act for IRAs up to ~$1.5M)

- BUT this protection applies in bankruptcy. If you don’t file bankruptcy and the lender gets a judgment, state law determines what they can seize. Some states protect retirement accounts from judgment creditors. Some don’t.

- Rollover as Business Startup (ROBS) — if you used retirement funds to capitalize the business, that money already left the protected account and is now business equity. It’s gone if the business fails.

Other assets

- Vehicles in your name

- Investment properties or rental real estate

- Equipment, boats, recreational vehicles — anything with a title

- Business interests in other companies you own

Your spouse’s assets in community property states

This is where it gets serious for married buyers. Nine states follow community property rules: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

In these states, most assets acquired during the marriage are jointly owned — regardless of whose name is on the account. That means your spouse’s savings, their share of the equity in the house, even their separate income could be exposed to your personal guarantee.

Even in non-community-property states (common law states), jointly owned assets like a co-titled house or joint bank account are still reachable.

Concrete example: a $900K SBA loan

Let’s put real numbers on this. You’re buying a $1.2M HVAC company:

- Purchase price: $1.2M

- SBA 7(a) loan: $900K (75% of purchase)

- Seller note: $180K (15%, on full standby)

- Your equity injection: $120K (10%)

Here’s what you’re personally guaranteeing: that $900K loan balance, plus interest. Over a 10-year SBA term at prime + 2.75% (call it 10.25% in today’s rate environment), you’ll owe approximately $1.4M in total payments. If you default in year three with a remaining balance of $780K, that’s the number they come after you for — personally.

Your personal financial snapshot:

- Home equity: $180K

- Savings: $45K (post-injection)

- 401(k): $210K (partially protected)

- Truck: $28K

That’s your exposure. All of it except the 401(k) is accessible to the lender if things go sideways.

Key Warning: The SBA requires the lender to take available collateral, including personal real estate, to secure the loan. Your home will likely have a lien placed on it at closing — not as a maybe, as a condition of the loan.

What Happens If the Business Fails

Nobody wants to talk about this part. But you need to understand the exact sequence of events if the business can’t service the debt. This isn’t fear-mongering — it’s the mechanical reality of default.

The timeline

Months 1–3 of missed payments: The lender contacts you. You work out a payment plan or forbearance. This is the window where you have the most leverage. Banks don’t want to liquidate — they want payments.

Months 3–6: If you can’t catch up, the lender sends a formal demand letter. The loan is classified as “in default.” They notify the SBA.

Months 6–12: Liquidation begins. The lender seizes and sells the business assets — trucks, equipment, inventory, the customer list (if it has standalone value), and any real property owned by the business.

After liquidation: The lender tallies the recovery. If they sold $500K worth of business assets against a $780K loan balance, there’s a $280K deficiency. That deficiency is your personal responsibility under the guarantee.

Deficiency judgment: The lender (or the SBA, after they’ve paid the lender under their guarantee) pursues a deficiency judgment against you personally. This is a court order that says you owe $280K and gives them the legal tools to collect it.

What collection looks like

Once they have a judgment, they can levy your bank accounts, garnish up to 25% of your disposable income, place liens on your home (preventing sale or refinance), and in some cases force the sale of non-exempt assets.

Real scenario

You bought a $1M HVAC company. SDE was $280K. You figured debt service of $155K/year was covered with room to spare. Then the company loses its biggest commercial contract (18% of revenue), two senior techs leave and take residential customers with them, and a mild winter cuts seasonal revenue by 30%.

Year two, the business generates $160K in SDE. Your debt service is $155K. You’re working for $5K a year before you pay yourself or cover the seller note.

Year three, you default. The lender liquidates. The trucks are worth less than you think (they always are). The customer list is eroded. Equipment depreciates fast. Total recovery: $420K against a $720K remaining balance.

You now personally owe $300K, plus legal and collection fees. Your credit score drops to the 500s. That debt follows you for years — the statute of limitations on a deficiency judgment varies by state but ranges from 6 to 20 years. In some states, they can renew the judgment.

This isn’t designed to scare you out of buying. The SBA default rate is around 15–20% over the life of the loan. Most of those people didn’t plan to fail. They just didn’t fully understand what they were risking.

Does Your LLC Actually Protect You? (Short Answer: No)

This is the single biggest misconception I encounter with first-time HVAC buyers. “I’ll set up an LLC, so my personal assets are protected.”

No. They are not. Not from the SBA loan.

Here’s the distinction:

- An LLC protects you from business liability. If a customer sues because your tech damaged their property, the LLC shields your personal assets from that claim. This is real protection and it matters.

- A personal guarantee explicitly bypasses that protection. That’s the entire point of the guarantee. The lender is saying: “We know you have an LLC. We don’t care. We want you, the person, on the hook.”

The personal guarantee doesn’t “pierce the corporate veil” in the legal sense. It’s not a failure of your LLC structure. It’s a separate, voluntary agreement where you personally agree to repay the debt. Your LLC is still intact. It just doesn’t help you with this particular obligation.

Think of it this way: the LLC is a firewall between the business and your personal life. The personal guarantee is a door you install in that firewall and hand the lender the key.

The LLC still protects you from business liability — slip-and-fall lawsuits, vehicle accidents, customer disputes, employee claims. That matters. But for “what happens if I can’t pay the SBA loan,” the LLC does nothing.

Key Warning: Some buyers think forming an S-Corp or C-Corp instead of an LLC provides better protection from a personal guarantee. It doesn’t. The personal guarantee is a separate contract that sits outside your entity structure entirely.

How to Reduce Your Exposure (Within the System)

You can’t avoid the personal guarantee on an SBA loan. But you can make it less dangerous. Here’s how, in order of impact.

1. Negotiate the collateral requirements with your lender

The SBA requires the lender to collateralize the loan with available business and personal assets. But there is flexibility in how aggressively the lender pursues personal collateral.

Some lenders will:

- Accept a lien on the business assets only, if the business has sufficient collateral

- Limit the personal lien to your primary residence and not pursue secondary assets

- Agree to release personal collateral after a certain percentage of the loan is paid down

This varies by lender. A lender who specializes in SBA acquisition loans will be more flexible than a community bank doing their first one. Shop around.

2. Maximize seller financing to reduce the SBA loan amount

Every dollar the seller carries is a dollar you don’t personally guarantee to the SBA. A deal structured with 30% seller financing and a $630K SBA loan has meaningfully less personal exposure than a deal with 75% SBA financing at $900K.

Seller notes typically don’t require personal guarantees (though some sellers ask for them). Even when they do, the seller’s recourse in a default is usually limited to the business assets — they’re not coming after your house.

3. Know your state’s homestead exemption

Homestead exemptions protect some or all of your home equity from creditors. The variation between states is enormous:

- Texas and Florida: Unlimited homestead exemption (your primary residence is protected regardless of value)

- California: $300K–$600K depending on county median home price

- Nevada: $605K

- Ohio: $145,425

- New Jersey: $0 (no homestead exemption)

If you’re in Texas or Florida, your home is largely protected even if everything else goes sideways. If you’re in a state with a low or zero exemption, your home is fully exposed.

Key Warning: Homestead exemptions protect equity from judgment creditors, but a voluntary lien is different. If the lender requires a mortgage/deed of trust on your home as collateral for the SBA loan (which they often do), the homestead exemption may not help you. The exemption protects against involuntary liens, not voluntary ones you agreed to at closing.

4. Keep personal assets rigidly separate

Do not co-mingle personal and business funds. No personal expenses through the business, no undocumented transfers. Clean separation won’t prevent the guarantee from being enforced, but it protects your LLC’s liability shield for non-guarantee claims and limits what a lender can easily identify and reach.

5. Get a life insurance policy sized to the guarantee

A term life insurance policy covering the loan amount costs relatively little and protects your family from inheriting your debt obligations. If you die, the policy pays off the loan and the guarantee becomes irrelevant.

For a $900K term policy on a healthy 35-year-old, you’re looking at $50–$80/month. That’s a rounding error in the context of this deal.

Most SBA lenders require life insurance on the borrower anyway. Make sure the coverage amount matches the loan balance, not a lesser amount.

6. Build equity fast and refinance

The guarantee stays until the loan is paid off. Apply excess cash flow to principal in years 1–3, grow the business value, and target a conventional refinance at the 3–5 year mark. Some lenders will consider releasing the personal guarantee once the loan-to-value ratio drops below 60–70%. A $1.2M acquisition that’s worth $1.8M in three years has real refinancing leverage.

The Conversation You Need to Have With Your Spouse

If you’re married, there is a conversation you must have before you sign. Not after. Not “when the time is right.” Before.

This isn’t about getting permission. It’s about making sure the person who shares your financial life understands exactly what’s at stake — because they’re at stake too.

What your spouse needs to know

Walk through these points together. Use real numbers from your actual financial situation.

- The total personal guarantee amount and what it means (everything above)

- Which specific assets are exposed — the house, the savings, the joint accounts

- Community property implications if you’re in a community property state

- Whether they need to co-sign (if they own 20%+ of the business, they must)

- The worst-case scenario: the business fails, the assets are liquidated at a loss, and you owe $200K–$400K personally. What does that look like for your family? Can you recover?

The gut-check framework

Before you sign, answer these together:

- Would you bet your house on this specific business? Not on your skills. Not on the HVAC industry. On this company, with these financials, in this market.

- If you lost the house, could your family recover within 5 years? Do you have income-earning ability outside this business?

- Is there a number where you walk away? If the loan were $1.5M instead of $900K, would you still sign?

If you and your spouse can’t align on these questions, that’s important information. It doesn’t mean don’t do the deal — but it means you haven’t reached a shared understanding of the risk yet.

Key Warning: In community property states (AZ, CA, ID, LA, NV, NM, TX, WA, WI), your spouse’s assets can be pursued to satisfy your personal guarantee even if they never signed anything. This isn’t optional knowledge — it’s a legal reality that affects the entire household.

When the Risk Is Worth It (And When It Isn’t)

Every acquisition carries risk. The personal guarantee just makes that risk personal. The question isn’t whether the guarantee is scary — it is — but whether the business you’re buying justifies the exposure.

The math that makes it manageable

The single most important number is the debt service coverage ratio (DSCR). This is the business’s available cash flow divided by the annual loan payment.

- DSCR of 1.25x or higher: The business generates $1.25 in cash flow for every $1.00 in debt service. This is the SBA’s minimum, and it’s a reasonable floor.

- DSCR of 1.5x or higher: You have a meaningful cushion. The business can absorb a bad quarter and still make payments.

- DSCR below 1.25x: The math doesn’t work. Don’t talk yourself into it with projections about how you’ll grow revenue. Base the decision on what exists today.

For a $900K SBA loan at 10.25% over 10 years, your annual debt service is roughly $145K. At a DSCR of 1.25x, you need $181K in available cash flow (SDE minus your reasonable salary). At 1.5x, you need $218K.

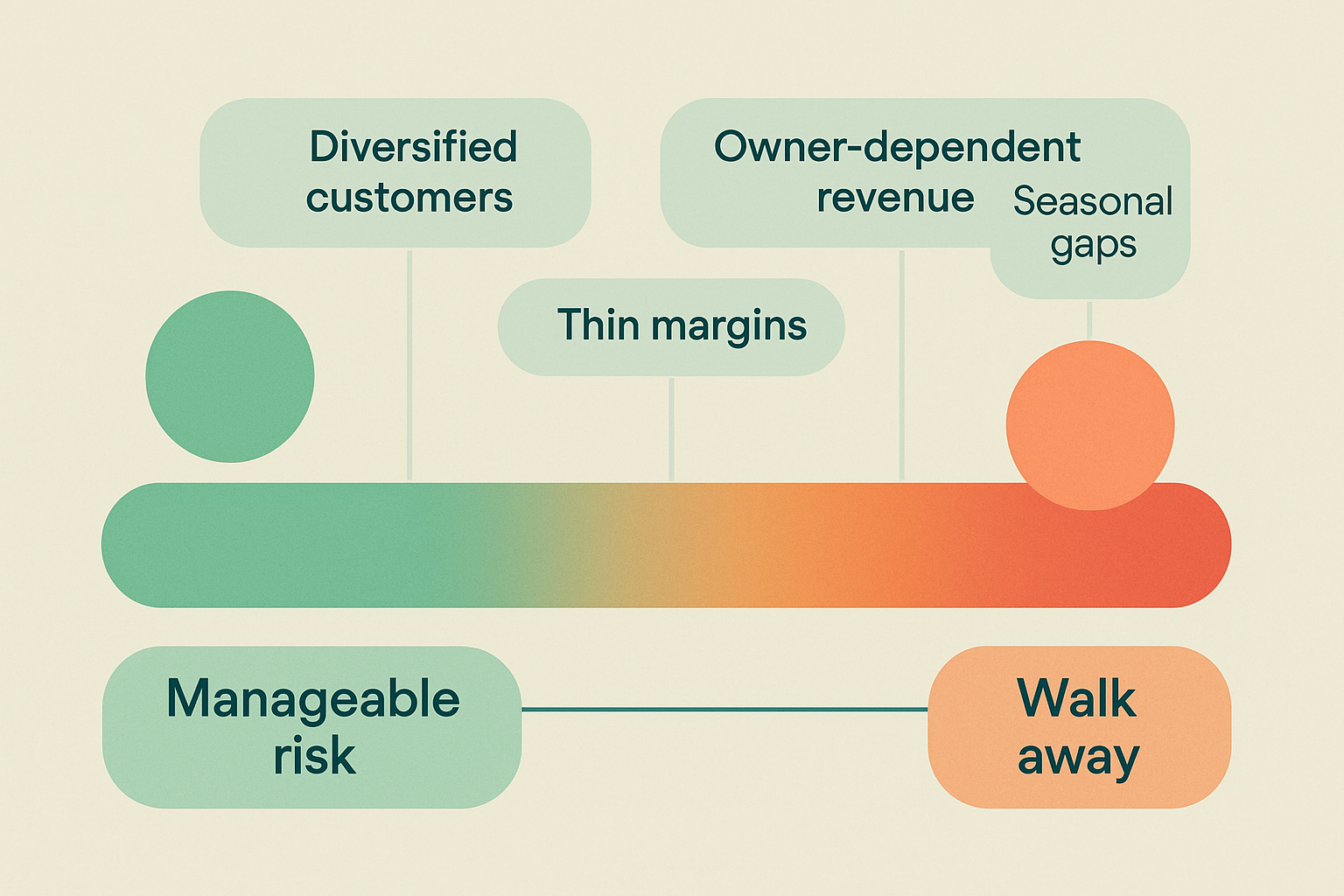

Signs the guarantee risk is tolerable

- Strong recurring revenue: 30%+ of revenue comes from maintenance agreements and repeat customers. This creates a floor under cash flow.

- Diversified customer base: No single customer accounts for more than 10% of revenue. Losing one contract doesn’t sink the ship.

- Healthy gross margins: 50%+ on service work, 30%+ on installations. There’s room to absorb cost increases.

- Multiple revenue streams: Residential service, commercial contracts, new installations, maintenance agreements. If one segment slows, others carry the load.

- Stable workforce: Techs have been there 3+ years. You’re not buying a revolving door that’ll empty out when the owner leaves.

Signs to walk away

- Owner-dependent revenue: The owner personally handles the top 20 accounts and those customers are loyal to the person, not the company. When the owner leaves, so does the revenue.

- Seasonal cash flow that barely covers debt: If June through September covers the annual debt service and the other eight months are a prayer, one cool summer destroys you.

- Thin margins with no pricing power: If the company competes on price in a crowded market, margins will compress further. You can’t guarantee your way out of a race to the bottom.

- Deferred maintenance on the fleet and equipment: Trucks with 200K miles, recovery machines from the Clinton administration, no investment in tools or technology for years. You’ll be spending cash on catch-up instead of debt service.

- Concentrated revenue: One commercial contract is 25% of revenue. When that contract goes to bid next year, so does your financial future.

The real question

Here’s how I frame it for every buyer I talk to:

Can this business survive losing its best month?

Take the highest-revenue month of the year. Delete it. Replace it with the worst month. Now run the numbers. Can you still make debt service? Can you still make payroll? Can you still pay yourself?

If yes, the personal guarantee is a calculated risk on a solid business. Sign it, work hard, pay it down, and refinance in five years.

If no, the business is too fragile to absorb the kind of disruption that every HVAC company eventually faces. A mild winter, a lost contract, a refrigerant price spike, a tech shortage — something will hit. The question is whether the business can take the punch.

Don’t bet your house on a business that can’t take a punch.

Frequently Asked Questions

Can I negotiate to remove the personal guarantee on an SBA loan?

No. It’s a program-level requirement, not a lender decision. You can negotiate collateral terms, but the guarantee itself is non-negotiable.

Does my spouse have to sign the personal guarantee?

Only if they own 20%+ of the acquiring entity. But in community property states, the lender may require spousal consent because marital assets are jointly owned. Even without signing, your spouse’s shared assets may be exposed.

What happens to the guarantee if I sell the business?

It stays until the SBA loan is paid off. If you sell and pay off the loan with proceeds, it terminates. If the buyer assumes the loan, you may remain on the guarantee unless the lender releases you in writing. Get that release before closing.

Can I file bankruptcy to escape the personal guarantee?

Bankruptcy can discharge guarantee obligations, but it destroys your credit for 7–10 years and makes future business financing extremely difficult. Last resort, not a strategy.

Is there a way to get an SBA loan without a personal guarantee?

No. You can reduce exposure by maximizing seller financing, increasing your equity injection, or pursuing non-SBA lenders (some offer limited or no personal guarantees, though rates are higher and terms shorter).

How much does it cost to have an attorney review the guarantee?

$500–$1,500. This is not optional. An attorney can identify negotiable collateral terms and explain your homestead and retirement protections under state law.

The Bottom Line

The personal guarantee is the price of admission for SBA-financed acquisitions. You can’t avoid it, but you can understand it, prepare for it, and structure the deal to minimize your downside.

The buyers who get hurt are the ones who treat the guarantee like a formality — one more signature in a stack of papers. It’s not. It’s you telling a federal agency that you’ll cover a six- or seven-figure debt with everything you own.

Understand the exposure. Have the conversation with your spouse. Know your state’s protections. Size the deal so the business can service the debt with room to spare. And if the numbers only work when everything goes right, walk away. There will be another deal.

The guarantee should be the last thing that scares you — not because it isn’t serious, but because by the time you sign it, you should have already done enough homework to know the risk is worth taking.

Understanding how SBA financing works in the bigger picture? Start with the HVAC acquisition math guide for deal structure fundamentals. If you’re weighing SBA vs. seller-carried options, the seller financing guide covers alternative structures. And for seasonal cash flow stress testing, the off-season cash flow guide walks through the numbers that determine whether debt service is sustainable.