You don’t need 10% cash to close an SBA-financed HVAC acquisition anymore. The 2026 standby rules created a dual seller note structure that cuts your cash requirement in half — if you know how to use it.

Most first-time HVAC buyers hear “SBA loan” and immediately do the math: 10% down on a $1.2M company means $120,000 in cash. That’s the number that kills most deals before they start. A technician earning $75K-$95K a year doesn’t have six figures sitting in a savings account.

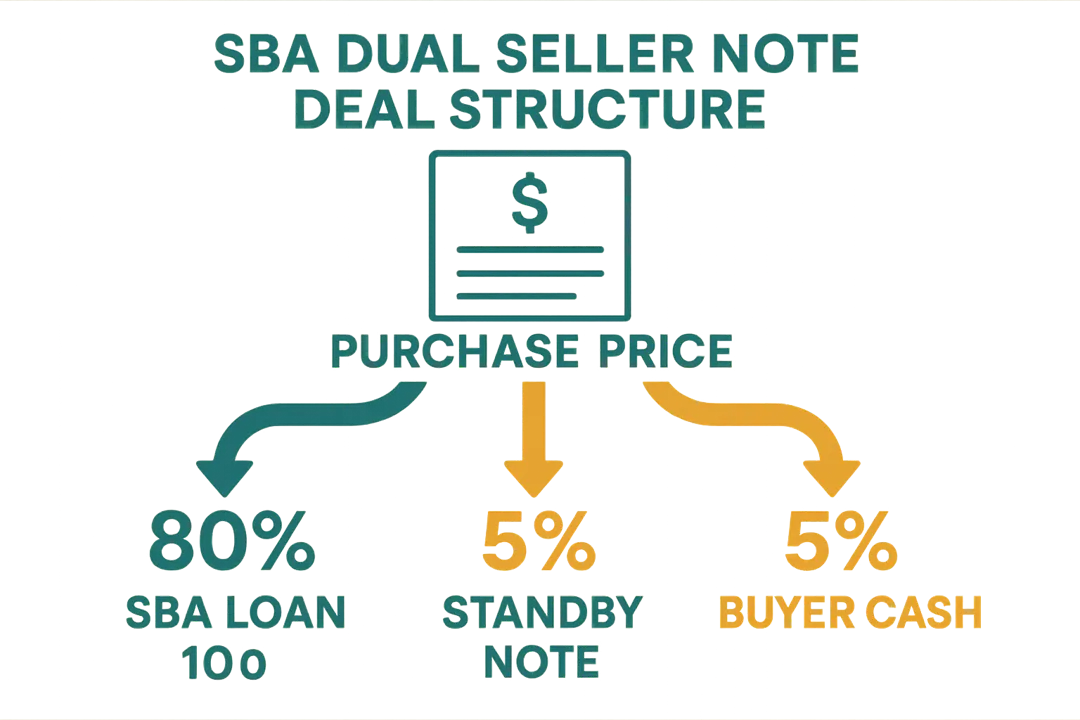

But the SBA’s 2025-2026 rule changes created a financing structure that most buyers — and plenty of brokers — still don’t fully understand. It’s called the dual seller note, and it can drop your cash-to-close from $120,000 to $60,000.

Here’s exactly how it works.

The Old Rules vs. The New Rules

Before the 2025 SBA SOP update, buyers needed a full 10% equity injection in cash. Seller notes could exist alongside an SBA loan, but they couldn’t count toward that 10%.

The new rules changed one critical provision: a seller note on full standby can now count toward up to half of the required equity injection.

That means on a $1.2M HVAC acquisition:

- Old structure: $120,000 cash from buyer + $960,000 SBA loan + optional seller note

- New structure: $60,000 cash from buyer + $60,000 standby seller note + $960,000 SBA loan + optional second seller note

Same purchase price. Half the cash.

What “Full Standby” Actually Means

This is where most explanations get vague. Here’s what full standby requires under the current SBA SOP:

- No payments — principal or interest — for the entire life of the SBA loan (typically 10 years for a business acquisition)

- Fully subordinated to the SBA loan — the SBA gets paid first, always

- No acceleration clauses — the seller can’t call the note due early for any reason

- No default triggers tied to the SBA loan — if you miss an SBA payment, the seller can’t use that to demand their money

In practical terms: the seller agrees to lend you $60,000, receives nothing for 10 years, and only gets repaid after the SBA loan is fully satisfied. It’s not a loan in any meaningful sense during those 10 years — it’s deferred consideration.

The Second Note: Where the Seller Actually Gets Paid

Here’s the part that makes the deal work for sellers who aren’t willing to wait a decade for $60,000: the second seller note.

Nothing in the SBA rules prevents a seller from carrying a second note with conventional payment terms — as long as it’s separate from the standby note and the combined debt service is feasible.

A typical dual note structure on a $1.5M HVAC acquisition looks like this:

| Component | Amount | Terms |

|---|---|---|

| SBA 7(a) loan | $1,200,000 (80%) | 10-year, Prime + 2.75%, ~$13,800/mo |

| Standby seller note | $75,000 (5%) | Full standby, 10 years, 0% |

| Conventional seller note | $150,000 (10%) | 5-year, 6%, ~$2,900/mo |

| Buyer cash | $75,000 (5%) | — |

The seller walks away from closing with $1,200,000 in cash (the SBA proceeds), starts receiving $2,900/month on the conventional note immediately, and has $75,000 deferred for 10 years. The buyer puts up $75,000 instead of $150,000.

Why Sellers Agree to This

The obvious question: why would a seller accept $75,000 in deferred money they can’t touch for a decade?

Three reasons:

- It closes the deal. A buyer who can’t produce $150,000 in cash walks away. A deal that closes at a slightly worse structure beats a deal that dies. Most HVAC sellers over 60 have been trying to exit for 2-3 years — they want to be done.

- The total proceeds are the same. The seller still gets $1.5M. The timing on $75,000 shifts, but the total number doesn’t change. For a seller receiving $1.2M in cash at closing, $75,000 deferred is a rounding error on their retirement plan.

- It’s standard practice now. SBA lenders are actively structuring deals this way. It’s not a creative negotiation tactic — it’s a published, documented SBA program feature. Sellers’ attorneys are familiar with it.

The Conversation With Your Lender

Not every SBA lender handles dual notes the same way. Here’s what to ask:

- “Do you allow standby seller notes to count toward equity injection?” — If they say no or seem confused, find a different lender. Preferred Lenders process this without SBA approval delays.

- “What’s your maximum conventional seller note as a percentage of the deal?” — Most lenders cap total seller financing (standby + conventional) at 15-20% of the purchase price. Some go higher if cash flow supports it.

- “How do you underwrite the combined debt service?” — The SBA loan payment plus the conventional seller note payment must fit within the business’s debt service coverage ratio (typically 1.25x). The standby note doesn’t count because there are no payments.

- “What documentation do you need from the seller?” — The standby note has specific SBA-required language. Your lender will provide the template. Don’t let the seller’s attorney draft it from scratch — it will get bounced.

If you’re still evaluating lenders, our guide on choosing the right SBA lender covers how to identify Preferred Lenders with experience structuring seller note deals.

When This Structure Doesn’t Work

The dual note isn’t magic. It fails when:

- The seller won’t accept any deferred consideration. Some sellers — particularly those advised by divorce attorneys or estate planners — need 100% at closing. No negotiation will change that.

- The business can’t support the combined debt service. On the $1.5M example above, total monthly payments are ~$16,700. That requires roughly $250,000 in annual seller’s discretionary earnings to meet the 1.25x coverage ratio. If the business only generates $180K SDE, the math doesn’t work regardless of how you structure the notes.

- You can’t produce even 5% cash. The SBA’s minimum buyer cash injection is now 5% — non-negotiable. On a $1.2M deal, that’s $60,000. If you don’t have $60,000, you need to either find a less expensive acquisition target or explore alternative financing paths.

- The seller has existing liens that consume the full purchase price. If the SBA proceeds go entirely to paying off the seller’s debts, there’s nothing left for them — and asking for an additional deferred note on top of that is a non-starter.

The Step-By-Step: Structuring a Dual Note Deal

If you’re a first-time HVAC buyer with $60K-$80K in accessible capital, here’s the sequence:

- Get SBA pre-qualified before you start searching. Know your buying power. A pre-qualification letter tells sellers you’re real.

- Target acquisitions at 10-15x your cash. With $75K in cash and a dual note structure, you can pursue deals up to $1.5M. With $60K, stay under $1.2M.

- Bring it up early in the LOI. Don’t surprise the seller at closing. The letter of intent should specify: “Purchase price of $X, financed via SBA 7(a) loan, buyer cash injection of 5%, standby seller note of 5%, and conventional seller note of X%.”

- Use a Preferred Lender. They can approve the structure without sending it to the SBA for secondary review, which saves 2-4 weeks.

- Get the standby note language right the first time. SBA has specific requirements for standby note documentation. Your lender provides the template. Using the wrong language is the #1 reason these structures get rejected at underwriting.

What This Means for HVAC Technicians Ready to Buy

The 2026 SBA rules didn’t just tweak the paperwork — they fundamentally changed who can afford to buy an HVAC company. A lead installer earning $85K who has saved $65,000 over five years can now pursue acquisitions up to $1.3M. That covers most single-location HVAC operations with $800K-$1.5M in revenue.

The bottleneck moved. It’s no longer “can you come up with the cash?” It’s “can you find the right deal and structure it correctly?”

If you’re navigating the SBA process for the first time, Lendesca specializes in helping first-time business buyers work through exactly these kinds of financing structures — matching you with the right lender and ensuring the deal mechanics actually close.

The money is more accessible than it’s ever been. The question is whether you know how to ask for it.

The SBA standby seller note rules are governed by SOP 50 10 8, effective for all 7(a) loans originated after July 2025. Rules may change — verify current requirements with your lender before structuring a deal.

For more on seller financing fundamentals and how they interact with SBA loans, see our full guide.