Estate-triggered acquisitions are some of the best deals in HVAC — and some of the most dangerous. Here’s how to navigate them.

The listing wasn’t on BizBuySell. It came through a probate attorney who called your business broker: “My client’s husband owned an HVAC company. He died three months ago. The company is still running — barely. The family needs to sell.”

You’re going to hear some version of this more often than you’d expect. And if you know how to handle it, you’ll find yourself looking at a deal with motivated sellers, no competing PE offers, and a business that — with the right timing — still has real value underneath the chaos.

But get it wrong, and you’re buying a shell.

Why Estate Sales Happen More Than You Think

The average HVAC business owner is north of 51 years old. That’s not a guess — that’s SCORE data backed up by every industry survey out there. These are guys who started their shops in their 30s, ground through two decades of 5 a.m. calls and August attics, and never quite got around to planning what happens next.

Here’s the ugly number: more than 70% of small businesses have no succession plan. No buy-sell agreement. No designated successor. No instructions beyond “the QuickBooks password is taped to the monitor.”

Death isn’t the only trigger. Disability and divorce force sales too. But death is the most abrupt — zero transition, zero warning, and a family that suddenly owns a business they don’t understand.

The takeaway for you as a buyer: probate attorneys and estate planners are massively underused off-market deal sourcing channels. Most buyers are refreshing BizBuySell listings. Smart buyers are having coffee with the trust-and-estates lawyers in their market.

The Legal Framework: Probate vs. Trust vs. Buy-Sell Agreement

Before you start running numbers, you need to know what legal structure you’re dealing with. It determines who you negotiate with, how long it takes, and whether the deal can happen at all.

Sole Proprietorship

The business doesn’t legally survive the owner. All assets pass through probate. The “company” ceases to exist — you’re buying assets (trucks, tools, customer list, phone number) from an estate.

This is the messiest scenario. Probate can take months, and nobody has legal authority to run the business in the meantime.

LLC

Check the operating agreement. Some LLCs have provisions for member death — surviving members may have buyout rights or the agreement may require dissolution. If the deceased was the sole member, the LLC interest passes to the estate, and you negotiate with the executor or administrator.

Key question: does the operating agreement address death of a member? If it doesn’t, you’re in state-default territory, and that varies wildly.

Corporation With Buy-Sell Agreement

If the deceased had partners and they had a buy-sell agreement, the surviving owners likely have right of first refusal. You may be waiting on them to pass before you get a shot.

Ask about this early. Don’t burn three weeks on diligence only to discover the partner is exercising their buyout clause.

Trust-Held Business

If the business was held in a living trust, you negotiate with the trustee — not the family. This can actually be cleaner. Trustees have legal authority to act, don’t need court approval for every decision, and are generally more businesslike in negotiations.

Regardless of structure, expect court approval to add 60 to 120 days to your acquisition timeline. Budget that into your planning from day one.

The Deterioration Clock: What Happens to an HVAC Business Without Its Owner

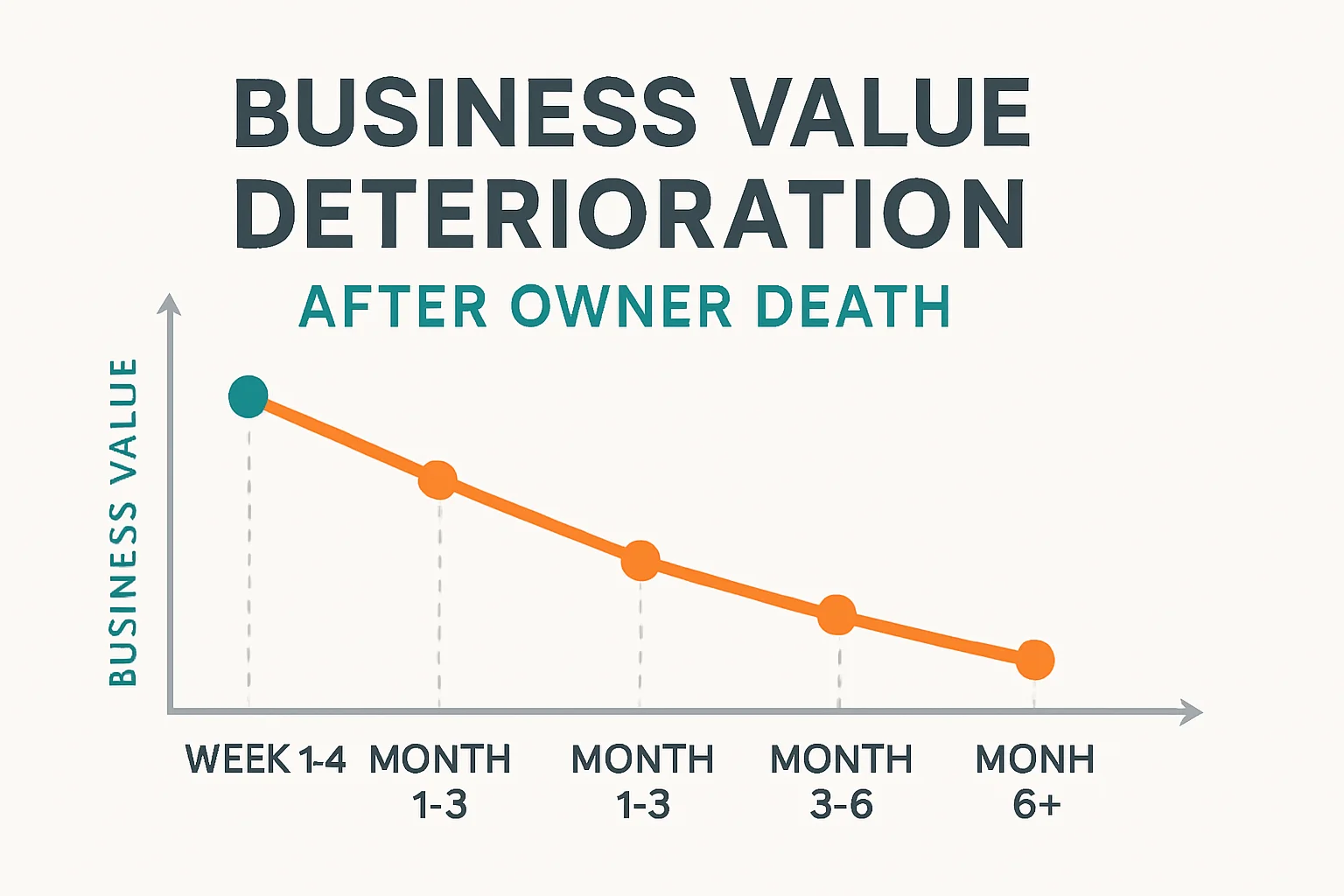

This is the part that makes estate deals simultaneously attractive and terrifying. An HVAC company without its owner degrades on a predictable schedule, and the clock starts the day they die.

Weeks 1–4: The Whisper Phase

- Key employees get nervous. The lead tech starts taking calls from recruiters.

- The office manager holds things together on muscle memory.

- Customers calling in don’t notice much yet.

Months 1–3: The Wobble

- Your best techs start interviewing. Competitors are circling — they know exactly what happened.

- Customers who call and hear “we’re under new management… sort of” start looking elsewhere.

- Dispatching gets sloppy. Nobody’s managing callbacks or upsells.

- Run the owner dependency test mentally — if the answer is “this guy WAS the business,” the clock is ticking faster.

Months 3–6: The Slide

- Service agreements start lapsing. Renewals don’t go out because nobody knows the process.

- Fleet maintenance gets deferred. That van with 190K miles doesn’t get replaced.

- Vendor credit tightens. Distributors who extended terms based on a handshake want to see the new situation.

Month 6+: The Remains

At this point, you’re not buying a business. You’re buying a customer list, some trucks, and maybe a phone number with local recognition. The SBA guidance on business transfers doesn’t sugarcoat this — the longer a business sits without leadership, the less there is to transfer.

Speed matters more in estate deals than any other acquisition type. Every week you delay, value walks out the door — sometimes literally, in a tech’s pickup truck.

Negotiating With Executors, Trustees, and Grieving Families

This is where the human element gets real. You’re sitting across from someone whose spouse or parent just died, and you’re talking about EBITDA multiples. Handle it wrong and the deal dies. Handle it right and you’ll close faster than you would with a living seller.

Understand the Executor’s Position

Executors have a fiduciary duty to get fair value for estate assets — but they also have a duty to avoid further losses. A business bleeding $15K a month in overhead with declining revenue is a liability, not an asset. The executor knows this, even if the family doesn’t.

Expect Emotional Anchoring

The family will anchor to the business’s best year. “Dad always said the company was worth a million dollars.” Maybe it was — in 2019, when he was running it. That’s not what you’re buying today.

Be respectful but direct. Bring comps. Bring the actual financials. Show them what buying from a motivated seller typically looks like in terms of pricing versus peak valuations.

Work Through the Estate’s Attorney

This sounds counterintuitive, but the estate’s attorney is your ally, not your adversary. They understand:

- The business is depreciating daily

- The estate has carrying costs (payroll, rent, insurance)

- A clean sale is better than a drawn-out process

- Their fee comes from closing, not from stalling

Patience and empathy close faster than aggressive negotiation. The buyer who shows up respectful, organized, and ready to move gets the deal. The buyer who lowballs a widow doesn’t.

Due Diligence Adjustments for Estate Sales

Standard diligence applies, but estate deals have unique landmines. Adjust your process for these realities.

Financial Records May Be Incomplete

Many owner-operators kept critical information in their heads. Pricing formulas, handshake deals with builders, verbal commitments to employees — none of it written down.

- QuickBooks and banking access may be locked behind the deceased’s credentials. Budget time (and possibly a forensic accountant) to reconstruct.

- Tax returns are your best friend. The IRS has copies even if the family doesn’t. IRS business transfer guidance outlines what records should exist.

- Credit card statements can fill gaps in expense tracking.

Employee Interviews Are Urgent

Talk to the lead tech and office manager immediately. They know:

- Which customers are actually loyal vs. which followed the owner personally

- What verbal promises were made about pay raises or promotions

- Where the bodies are buried (figuratively — the deferred maintenance, the angry customer, the truck that needs a transmission)

Insurance Status

This is a major trip wire. Check immediately:

- Was there key person life insurance? If so, who’s the beneficiary — the business or the family?

- Is the company’s general liability still active, or did it lapse when the premium wasn’t paid?

- Workers’ comp: is it current? Check insurance transfer gaps thoroughly — a lapse in coverage during transition can be catastrophic.

Hidden Commitments

The family probably doesn’t know about:

- Pending install commitments or quoted jobs

- Equipment on order from distributors

- Verbal agreements with subcontractors

- Warranty obligations on recent installs

You need to find all of these before you sign anything.

Structuring the Deal

Asset Sale Is Almost Always the Answer

In estate acquisitions, you want an asset purchase — not a stock or membership interest purchase. You’re cherry-picking the valuable assets (customer list, service agreements, equipment, vehicles, phone numbers, trade name) and leaving behind any unknown liabilities.

The estate’s attorney will likely agree. They want clean separation too.

SBA Lending Works Here

SBA lenders see estate-triggered deals regularly. It’s not exotic. The BizBuySell estate sale guide confirms these transactions happen across every industry.

What lenders will scrutinize:

- Business continuity risk — who’s been running it, and will they stay?

- Revenue trajectory — is it declining, and how fast?

- Customer concentration — did the owner personally hold the key relationships?

Seller Financing Complications

In a normal deal, you’d negotiate a seller note for 10–20% of the purchase price. In an estate deal, the “seller” is a legal entity managed by an executor or trustee. Seller financing requires court or trustee approval, which adds complexity and time.

It’s doable but plan for it.

The Transition Gap

Here’s the biggest structural problem: who provides transition consulting when the owner is gone?

In a standard acquisition, the seller sticks around for 3–6 months to introduce you to customers, explain the quirks, and transfer relationships. That’s not possible here. You need to solve for this with:

- Extended retention bonuses for key employees who can fill the knowledge gap

- Customer outreach plan that’s aggressive and personal

- Vendor relationship rebuilding — show up at the distributor counter in person

For estate acquisitions where traditional seller involvement isn’t possible, working with a lending partner like Lendesca who understands non-standard deal structures can help you navigate financing that accounts for the missing seller note and the additional working capital you’ll need to stabilize the business post-close.

Valuation Realities

Estate deals typically close at a discount to market. That’s not you being predatory — it’s math:

- No seller transition reduces value by 10–15%

- Employee flight risk reduces value further

- Revenue decline during the ownership gap is real

- Incomplete records increase your risk premium

A business that might trade at 3x SDE with a cooperative seller transition might be worth 2–2.5x in an estate scenario. Fidelity’s estate planning guide reinforces why advance planning matters — and why the absence of it costs the estate money.

How to Position Yourself to Find Estate Deals

You don’t wait for these deals to find you. You build the network that surfaces them before anyone else hears about it.

Build Relationships With Probate Attorneys and Estate Planners

- Identify the 5–10 probate and trust attorneys in your market.

- Take them to lunch. Tell them exactly what you’re looking for: “If an HVAC or mechanical contractor comes through your practice as an estate asset, I’d like to be the first call.”

- Follow up quarterly. These are long-cycle relationships.

Tell Your Broker

Most business brokers default to listing-based deal flow. Tell yours explicitly: “I’m interested in estate situations, distressed deals, and anything that comes through probate channels.” You’re widening their aperture.

Monitor the Signals

- Trade association membership lapses — when a long-time member suddenly drops, something happened.

- License renewals that don’t happen — check your state licensing board periodically.

- Obituaries in trade publications — morbid but effective.

- Supply house chatter — distributors know when an owner dies before anyone else.

Be Known as the Fair Buyer

This is the long game. When you close an estate deal and treat the family well — pay a fair price, keep the employees, honor the legacy — word gets around. The next probate attorney who has a similar situation will remember the buyer who handled it with class.

Estate deals reward reputation. Build yours intentionally.

The Bottom Line

Estate-triggered HVAC acquisitions sit in a strange space: deeply human situations that require cold-eyed business analysis. The buyers who do well here bring both.

Move fast. Be respectful. Get the legal structure right on day one. Solve for the transition gap creatively. And build the relationships now — before the phone rings.

Because it will ring. In an industry full of aging owners with no succession plans, the math guarantees it.