You're about to buy an HVAC company. Before you argue over the price, before you line up financing, before you pick your closing date — you need to decide how you're buying it. Asset sale or stock purchase. Two structures. Wildly different consequences. And if you pick wrong, you could be writing checks for someone else's mistakes for years.

You've spent months finding the right HVAC business. The revenue looks solid, the trucks aren't falling apart, and the seller seems like a straight shooter. Your handshake is practically warm.

Then your attorney asks: “Are we structuring this as an asset purchase or a stock purchase?”

You nod like you know what that means. You don't. And that's fine — most first-time buyers don't. But this one decision will determine your tax bill for the next five to seven years, which liabilities follow you home, and whether you inherit that EPA complaint the seller forgot to mention. The tax difference alone can exceed $340K over five years on a $1M deal.

Let's fix the knowledge gap before it costs you real money.

Two Ways to Buy the Same Business — And They're Not Even Close

Here's the simplest way I can put this:

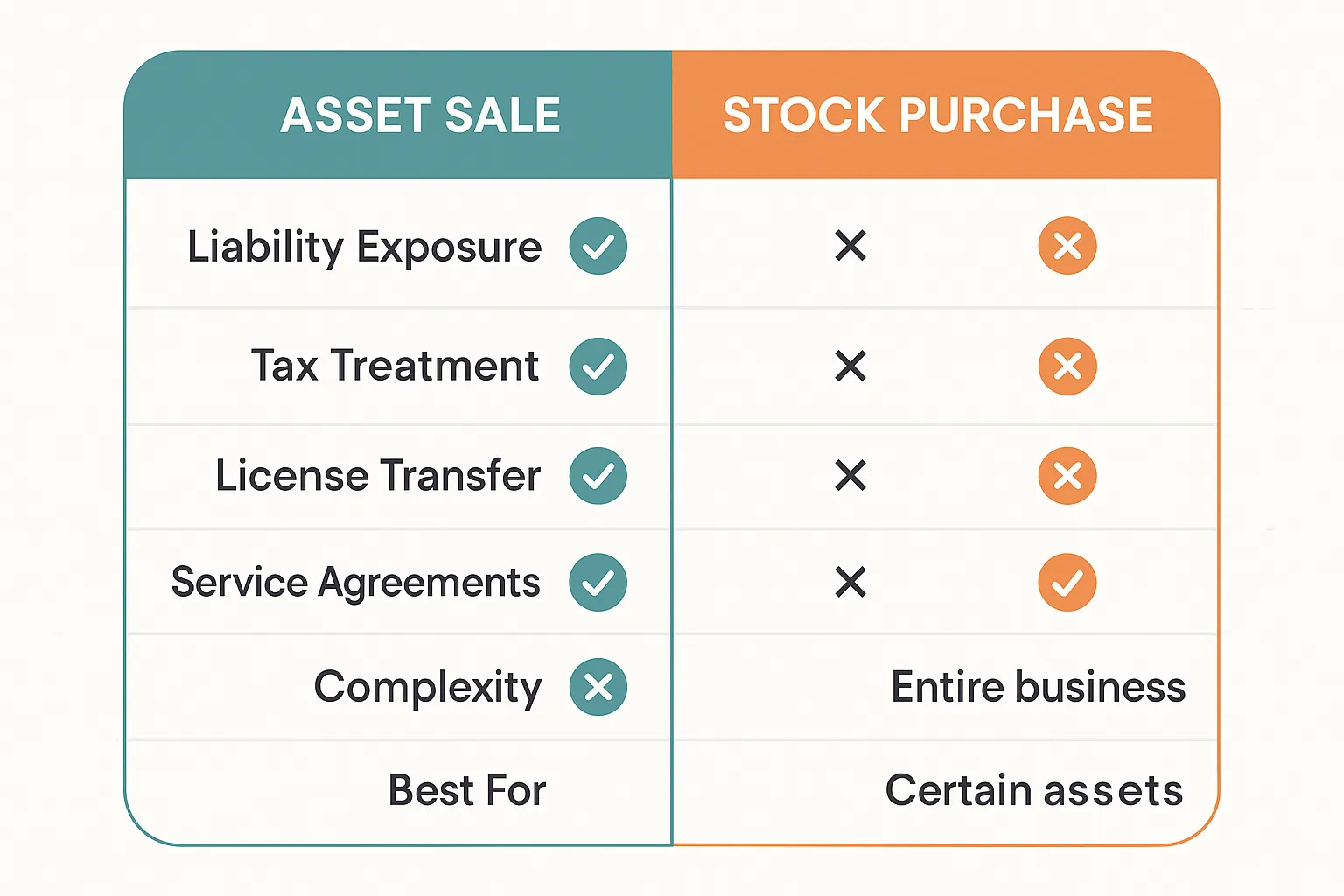

- Asset sale: You buy the stuff. The equipment, the trucks, the customer list, the brand name, the phone number. You're assembling a business from parts — parts you specifically chose.

- Stock purchase: You buy the company. The whole legal entity. Its EIN, its history, its contracts, its debts, its problems. Everything. You step into the seller's shoes, and those shoes might have nails in them.

Same business. Same revenue. Same trucks in the parking lot. But the legal, tax, and risk profiles are completely different depending on which structure you use.

Here's the number that should get your attention: roughly 85–90% of HVAC business sales under $5M are structured as asset sales. There's a reason for that. The buyers who went the other way learned some expensive lessons.

Spoiler: you almost certainly want an asset sale. The rest of this article explains why — and the rare situations where stock might make sense.

Asset Sale: What You're Actually Getting

In an asset sale, you and the seller sit down and agree on exactly which assets are changing hands. You're building a shopping list. If it's not on the list, it stays with the seller.

What you typically buy

- Vehicles and fleet — every van, truck, and trailer the business uses

- Equipment and tools — recovery machines, vacuum pumps, manifold sets, leak detectors, the whole shop

- Parts inventory — capacitors, contactors, blower motors, the stock room

- Refrigerant stock — R-410A, R-22 reclaim, whatever's on the shelf

- Customer lists and records — the database that drives repeat revenue

- Service agreements — maintenance contracts, planned service agreements, the recurring revenue engine

- Brand name and trade name — the DBA, the logo, the reputation

- Phone numbers — the number your customers have saved in their phones

- Website and digital assets — domain name, website, social media accounts

- Google Business Profile — the listing with 247 reviews and a 4.8-star rating

- Goodwill — the intangible value of the business beyond its hard assets

- Non-compete agreement — so the seller doesn't open a shop across the street

What you leave behind

This is the beauty of an asset sale. You get to walk away from:

- Outstanding debts and accounts payable

- Pending or threatened lawsuits

- Tax liabilities and back taxes

- That IRS audit from 2022 the seller keeps calling “no big deal”

- Workers' comp claims from before you showed up

- Environmental liabilities (usually — get this in writing)

- Contracts you don't want — that below-cost commercial maintenance deal the seller's brother-in-law negotiated

You're buying a business. You're not adopting its history.

Warning: “Leave behind” doesn't mean “automatically excluded.” Every asset and liability needs to be explicitly addressed in the purchase agreement. If it's not in the contract, you're rolling dice. Your attorney earns their fee here.

Stock Purchase: Why the Seller Wants It (And Why You Usually Don't)

In a stock purchase, you buy the seller's ownership interest in the company — their shares of stock (if it's a corporation) or their membership interest (if it's an LLC). The company continues to exist. Same EIN. Same contracts. Same everything.

Including same everything you didn't know about.

Why sellers push for stock sales

Simple: tax treatment. When a seller sells stock, the entire gain is typically taxed at the long-term capital gains rate — currently 20% for high earners, plus the 3.8% net investment income tax. That's it. Clean. One layer of tax.

In an asset sale, the seller faces a potential double tax problem if the business is a C-corp. The corporation pays tax on the asset sale, and then the seller pays tax again when the proceeds are distributed. Even for S-corps and LLCs, the allocation of purchase price to different asset categories can push some of the gain into ordinary income territory (depreciation recapture), which is taxed at higher rates.

So when a seller says “I really prefer a stock sale,” what they're saying is “I want to keep more of the money.” Fair enough. But their tax savings come at your expense — literally.

The risk you're inheriting

When you buy stock, you're stepping into the seller's legal shoes. You now own a company with its full history:

- Undisclosed liabilities — debts, claims, or obligations the seller didn't tell you about (or didn't know about)

- Tax exposure — if the company underreported income in 2021, that's your problem now

- Environmental issues — that refrigerant disposal situation from 2019? Yours

- Employment claims — the tech who got fired six months ago and is talking to a lawyer? Your company is the defendant

- Contract obligations — every agreement the company ever signed, good or bad

The horror story you need to hear

A buyer I know purchased a two-location HVAC company as a stock deal because the seller insisted — and gave a $75K price concession to sweeten it. Seemed like a win. Eighteen months later, a former employee filed a workers' comp claim alleging chemical exposure from a refrigerant leak in 2020. The claim, plus legal fees, plus the resulting OSHA inquiry, cost $180K.

That $75K “discount” turned into a $105K loss. The seller was on a beach in Florida. Legally, he had no obligation — the buyer owned the company and all its history.

Warning: Representations and warranties in the purchase agreement can offer some protection in a stock deal, but they're only as good as the seller's ability to pay an indemnification claim. If the seller spent the proceeds and has no assets, your indemnification clause is a piece of paper.

When a stock purchase might actually make sense

Stock deals aren't always wrong. They're just rarely right for sub-$5M HVAC acquisitions. Consider a stock purchase if:

- The company holds non-transferable government contracts (military base HVAC maintenance, federal facility agreements) that would terminate in an asset sale

- The business has licenses or certifications tied to the entity that can't be re-obtained — rare, but it happens in some states

- The entity owns real estate and transferring the property separately would trigger transfer taxes or reassessment

- The company has favorable long-term leases with assignment restrictions that the landlord won't waive

If none of those apply — and for most HVAC businesses under $5M, they don't — default to an asset sale.

The Tax Math That Makes Asset Sales Worth Fighting For

This is where the real money lives. In an asset sale, you get to “step up” the tax basis of every asset you purchase to its current fair market value. That means you can depreciate and amortize those assets from the price you paid — not from whatever the seller's old depreciated basis was.

In a stock purchase, nothing changes inside the company. The assets keep their old, already-depreciated basis. You bought a $1M business, but the company's books still show $120K in net asset value because everything was depreciated years ago.

Translation: you lose hundreds of thousands of dollars in tax deductions.

The $1M deal, two ways

Let's run real numbers on a $1M HVAC acquisition. Combined federal and state tax rate of 30%.

Asset sale allocation:

| Asset Category | Allocation | Depreciation/Amortization Period | Annual Deduction |

|---|---|---|---|

| Equipment (recovery machines, shop tools, diagnostic equipment) | $300,000 | 5–7 years | ~$50,000/yr |

| Vehicles (van fleet) | $150,000 | 5 years | $30,000/yr |

| Parts inventory | $75,000 | Expensed as sold | Varies |

| Customer list / service agreements | $125,000 | 15 years | ~$8,300/yr |

| Goodwill | $200,000 | 15 years | ~$13,300/yr |

| Non-compete agreement | $50,000 | Term of agreement (typically 3–5 years) | ~$12,500/yr |

| Other (phone numbers, website, brand) | $100,000 | 15 years | ~$6,700/yr |

| Total | $1,000,000 |

Year one with Section 179 and bonus depreciation:

In year one, you can potentially deduct the full cost of equipment and vehicles using Section 179 expensing (up to $1.16M in 2026) or bonus depreciation. That's up to $450K in deductions in year one alone.

At a 30% combined tax rate, that's $135K back in your pocket in the first year.

Stock purchase:

The company's assets are already depreciated on the books. You get... basically nothing new to write off. The old depreciation schedule continues as-is, which might be $15K–$20K per year of remaining depreciation.

Five-year comparison

| Asset Sale | Stock Purchase | Difference | |

|---|---|---|---|

| Year 1 deductions | ~$450,000 (Sec. 179) | ~$18,000 | $432,000 |

| Year 2 deductions | ~$40,000 | ~$15,000 | $25,000 |

| Year 3 deductions | ~$38,000 | ~$12,000 | $26,000 |

| Year 4 deductions | ~$35,000 | ~$10,000 | $25,000 |

| Year 5 deductions | ~$33,000 | ~$8,000 | $25,000 |

| Total additional deductions | ~$533,000 | ||

| Tax savings at 30% rate | ~$160,000 |

And those goodwill and customer list amortization deductions continue for 15 years. Over the full amortization period, the total tax benefit differential exceeds $340K.

That's not an abstraction. That's a truck. That's a year of payroll for a tech. That's your kids' college fund.

The seller negotiation

Sellers know this math — or their accountant does. Expect the seller to push back on an asset sale. Here's how to handle it:

- Acknowledge their concern. “I understand the asset sale creates a less favorable tax situation for you.”

- Quantify the difference. Have your CPA estimate the seller's additional tax burden from an asset sale vs. stock sale.

- Split the difference on price. If the asset sale costs the seller an extra $80K in taxes, consider increasing your offer by $30–40K. You're still coming out well ahead.

- Make it a deal term, not a dealbreaker. The structure is one piece of a larger negotiation. Trade on price, terms, transition period, or earnout — don't walk away over structure alone.

HVAC-Specific Wrinkles You Won't Find in Generic Guides

Every business acquisition guide covers asset vs. stock in the abstract. Here's what they miss about HVAC.

HVAC contractor licenses

This is the big one. In an asset sale, the seller's HVAC contractor license does not transfer to you. The license belongs to the individual or the entity — and you're not buying the entity.

What this means in practice:

- You need your own contractor's license before closing, or

- You need a qualifying individual (a licensed person willing to be your qualifier) lined up and approved by the state, or

- You negotiate a transition period where the seller stays on as the qualifier temporarily

In a stock sale, the company's license stays with the company. You own the company, so you effectively have the license. This is one of the few genuine advantages of a stock deal.

Warning: License requirements vary dramatically by state. Some states require the license holder to have an ownership stake. Some require the qualifier to be a W-2 employee. Some allow a temporary operating permit during transitions. Check your state's contractor licensing board before you sign a letter of intent. Not after. Before.

For a deeper look at license transfer mechanics, read our guide on the HVAC license trap.

Service agreement assignment

Your maintenance agreements are the crown jewel — recurring revenue that makes lenders and buyers drool. In an asset sale, those agreements technically need to be assigned to you, the new entity.

- Best case: The agreements include an assignment clause allowing transfer with notice to the customer

- Common case: Agreements are silent on assignment, requiring customer consent

- Worst case: Agreements include anti-assignment language, requiring renegotiation

Practically speaking, most residential HVAC customers don't care who owns the company as long as the same techs show up. But commercial contracts — especially with property management companies, HOAs, or municipalities — may have strict assignment provisions.

In a stock sale, the agreements stay with the entity. No assignment needed. The customer's contract is with ABC Heating & Cooling LLC, and ABC Heating & Cooling LLC still exists.

Google Business Profile

This one drives people crazy. Your GBP is worth real money — those reviews, that map placement, that search visibility. In a stock sale, the GBP stays with the business entity and nothing changes.

In an asset sale, you need to transfer the GBP. Google's official position on ownership changes is... let's call it “evolving.” Here's the practical playbook:

- Have the seller add you as an owner/manager of the GBP before closing

- After closing, have the seller transfer primary ownership to you

- Update the business information gradually — don't change everything at once

- Do not create a new listing. You'll lose everything.

It works. It's just annoying. Budget two to four weeks for the full transfer and don't expect Google support to be helpful.

Vehicle titles and registration

In an asset sale, every single vehicle needs an individual title transfer. For a company with eight service vans, two box trucks, and a trailer, that's eleven trips to the DMV (or your title service). Budget $200–$500 per vehicle for title transfer, registration, and new commercial insurance binding.

In a stock sale, the vehicles stay titled to the company. No transfers needed.

For a detailed look at insurance transfer during acquisitions, see our guide on insurance transfer gaps.

Refrigerant inventory and EPA compliance

If the business holds significant refrigerant inventory — especially R-22 reclaim — tracking requirements matter. The EPA requires records of refrigerant purchases, usage, and disposal tied to the certified entity.

In an asset sale, you need to:

- Document the transfer of refrigerant inventory with quantities and types

- Ensure your new entity has proper EPA Section 608 certification

- Transfer or re-establish refrigerant tracking records

- Update supplier accounts for refrigerant purchases

In a stock sale, the entity's EPA certifications and records stay intact.

Vendor and supplier relationships

Don't underestimate this one. In an asset sale, you may need to:

- Re-apply for distributor accounts (Carrier, Trane, Lennox, etc.)

- Re-establish credit terms — the seller had net-30 built over fifteen years. You're starting from scratch.

- Requalify for dealer programs and rebate tiers

- Update warranty registration portals

One buyer I talked to lost his Carrier dealer status for four months during the transition. That's four months of buying equipment at non-dealer pricing. It cost him roughly $35K in margin erosion before the account was sorted out.

Warning: Start the vendor transition process during due diligence, not after closing. Contact your key equipment distributors early. Some dealer programs have application windows, territory restrictions, or waiting periods that can blindside you at the worst possible time.

The Allocation Negotiation: Where the Real Money Is

If you're doing an asset sale (and you should be), the purchase price allocation determines how much tax benefit you actually capture. This isn't an afterthought — it's one of the most consequential negotiations in the entire deal.

Understanding how deal structure affects your total acquisition cost is critical — see our acquisition math guide for the full picture.

How it works

The total purchase price gets divided across asset categories. The IRS groups these into seven classes under Section 1060:

- Class I — Cash and cash equivalents

- Class II — Actively traded securities

- Class III — Debt instruments, accounts receivable

- Class IV — Inventory (parts, refrigerant stock)

- Class V — All other tangible and intangible assets (equipment, vehicles, customer lists, non-compete)

- Class VI — Section 197 intangibles other than goodwill (workforce in place, trade names, patents)

- Class VII — Goodwill and going-concern value

The allocation must be reasonable and reflect fair market value. Both buyer and seller must file Form 8594 (Asset Acquisition Statement) with their tax returns, and the allocations must match. If they don't, the IRS gets curious. You don't want the IRS to be curious.

What you want vs. what the seller wants

| Asset Category | Buyer Preference | Seller Preference | Why |

|---|---|---|---|

| Equipment | Maximize — 5-7 year depreciation | Minimize — depreciation recapture taxed as ordinary income | Faster write-off for buyer; higher tax for seller |

| Vehicles | Maximize — 5 year depreciation | Minimize — same recapture issue | Same dynamic |

| Inventory | Allocate at cost | Allocate at cost | Usually not controversial |

| Customer list | Moderate | Moderate | 15-year amortization for buyer; ordinary income for seller |

| Non-compete | Maximize — short amortization (3-5 years) | Minimize — ordinary income to seller | Big deduction for buyer over short period |

| Goodwill | Minimize — 15 year amortization (slowest) | Maximize — capital gains rate | Buyer gets slow deduction; seller gets favorable rate |

The tension is clear. You want more allocated to equipment, vehicles, and the non-compete (faster deductions). The seller wants more in goodwill (lower tax rate). This is a zero-sum game.

Practical allocation for a $1M HVAC deal

Here's a realistic middle-ground allocation that both sides can live with:

| Asset | Allocation | % of Total |

|---|---|---|

| Equipment and tools | $250,000–$325,000 | 25–33% |

| Vehicles | $125,000–$175,000 | 13–18% |

| Parts inventory | $50,000–$100,000 | 5–10% |

| Customer list / service agreements | $100,000–$150,000 | 10–15% |

| Non-compete agreement | $25,000–$75,000 | 3–8% |

| Trade name / phone / website | $25,000–$50,000 | 3–5% |

| Goodwill | $175,000–$300,000 | 18–30% |

The exact split depends on the actual fair market value of the assets — you can't just make up numbers. Get equipment appraised. Value the van fleet using NADA guides. Have a CPA or valuation professional support your allocation with documentation.

Three rules for the allocation negotiation

- Negotiate allocation before signing the purchase agreement. If the purchase agreement is silent on allocation, you'll be fighting about it after closing when leverage has shifted.

- Get it in writing as an exhibit to the purchase agreement. Not a handshake. Not a “we'll figure it out with our accountants.” A signed schedule.

- Support every number with documentation. Equipment appraisals, vehicle valuations, inventory counts, customer list analysis. The IRS doesn't audit vibes.

Which Structure to Choose — A Decision Framework

Let's make this simple.

Default: asset sale

Choose an asset sale unless you have a specific, documented, dollar-value reason to do otherwise. The tax benefits, the liability protection, and the clean-slate advantage are too significant to give up for convenience.

Consider stock if (and only if)

- The company holds government contracts that terminate on change of ownership and cannot be rebid

- The entity has licenses or certifications that are genuinely non-transferable and would take more than 90 days to re-obtain

- The company owns real estate where title transfer would trigger reassessment or transfer taxes exceeding $50K

- Equipment manufacturer dealer agreements have territory exclusivity that would be lost and re-awarded to a competitor

The hybrid approach

Some deals use a modified asset sale with additional protections:

- Asset sale + seller indemnification: The seller guarantees (backed by an escrow holdback) that no undisclosed liabilities exist. If something surfaces, the escrow covers it.

- Asset sale + transition services agreement: The seller stays on for 60–90 days as a consultant to help with license transfers, customer introductions, and vendor re-establishment.

- Asset sale + assumption of specific liabilities: You agree to assume certain known, quantified liabilities (like an outstanding equipment loan) in exchange for a lower purchase price.

Who needs to be in the room

This is not a DIY decision. Your team for the structure discussion:

- Acquisition attorney — not your buddy who does real estate closings. Someone who does M&A.

- CPA with deal experience — they model the tax impact of both structures. The fee pays for itself fifty times over.

- Business broker (if applicable) — they've seen how this negotiation plays out and can reality-check both sides

Budget $15,000–$25,000 for legal and accounting fees on a sub-$5M HVAC acquisition. That sounds like a lot until you remember the $180K environmental claim from the horror story above.

The one-line gut check

If you're still on the fence:

“Would I rather spend an extra $20K on legal fees and deal complexity now, or risk a $180K surprise next year?”

That's not a real question. You know the answer.

The Bottom Line

Deal structure isn't the exciting part of buying an HVAC business. It's not the trucks or the customer list or the moment you put your name on the building. But it's the decision that determines whether you're building wealth or cleaning up someone else's mess.

Asset sale. Step-up basis. Clean liability slate. Negotiate the allocation hard. Hire professionals who've done this before.

The seller will push back. That's fine. Pushback is a negotiation, not a wall. Find the price adjustment that makes both sides whole and close the deal on terms that set you up for the next twenty years — not terms that haunt you for the next five.

You're about to spend a lot of money. Make sure the structure is working for you, not against you.